Planning for Health Success

With recent changes to tax legislation, you can create and plan that truly supports your health care needs.

Maximize Your Health Savings: The HSA Advantage for DPC

Using your Health Savings Account (HSA) to pay for your monthly membership is like having a permanent "30% off" coupon for your healthcare. Because HSA funds are never taxed when used for medical expenses, you keep more of your hard-earned money in your pocket.

How the Savings Work

When you pay for your membership with an HSA, you save money in three distinct ways:

Federal Income Tax Discount: You avoid paying federal taxes on the money you spend on your health. Depending on your income, this is an immediate 10% to 37% savings.

The Payroll "Bonus" (FICA): If you contribute to your HSA through your employer’s payroll, you skip the 7.65% Social Security and Medicare tax. This is a unique benefit that even 401(k) plans don't offer!

Tax-Free Growth: Any money sitting in your HSA grows interest-free. You never pay taxes on the gains.

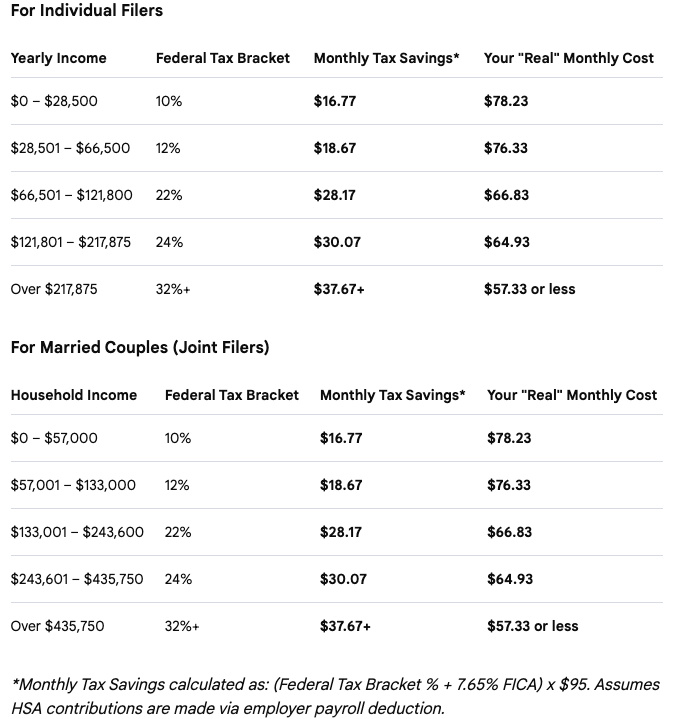

Savings Breakdown: What a $95 Membership Actually Costs

In New Jersey, while the state does not offer a specific deduction for HSA contributions, the Federal and Payroll savings are substantial. Below is what a $95 monthly membership feels like to your wallet after tax savings.

The Bottom Line

By using your HSA, you are effectively getting 3 to 5 months of your membership for free every year compared to paying with a regular bank card. Please do consult your own accountant.

Starting in 2026, HSAs and Direct Primary Care will finally work together!

Starting in 2026, HSAs and Direct Primary Care will finally work together!

In IRS Notice 2026-05, the IRS confirms that qualifying Direct Primary Care service arrangements can be used alongside HSAs, removing a longstanding barrier for patients who want both relationship-based primary care and tax-advantaged health savings.

Beginning January 1, 2026: DPC Will NOT Disqualify HSA Eligibility

Patients enrolled in a qualifying DPC arrangement may continue to contribute to an HSA, provided they are otherwise HSA-eligible (i.e., enrolled in a qualifying High-Deductible Health Plan).

Under prior IRS interpretations, DPC was often treated as “other coverage,” which could disqualify HSA contributions. That barrier is now removed.

HSA Funds MAY Be Used to Pay DPC Fees

The IRS now recognizes Direct Primary Care membership fees as eligible medical expenses, meaning:

Patients may use HSA dollars to pay DPC monthly or annual membership fees

Payments may be made tax-free from an HSA, beginning in 2026

This gives patients greater flexibility and affordability when choosing DPC.

What is an HSA?

An HSA (Health Savings Account) is like a special savings account designed specifically for medical expenses. Think of it as a piggy bank that the government gives you tax breaks for using - but only if you use the money for healthcare stuff.

How HSAs Work 🏥

You put money into the account (usually through payroll deduction)

The money can be used to pay for medical expenses like:

Doctor visits

Prescription medications

Dental care

Vision care

Medical equipment

Any money you don’t use stays in the account and grows over time

Why HSAs Are Beneficial 📈

Triple Tax Advantage (This is huge!)

Tax-deductible contributions: Money you put in reduces your taxable income

Tax-free growth: Any interest or investment gains aren’t taxed

Tax-free withdrawals: Money comes out tax-free when used for qualified medical expenses

Other Benefits:

The money never expires (unlike some other accounts)

It’s portable - you keep it even if you change jobs

After age 65, you can withdraw for any reason (though non-medical withdrawals are taxed like a regular retirement account)

Who Benefits Most? 🎯

Best for:

Healthy people who don’t have many medical expenses

High earners who want to reduce their tax bill

People planning for retirement (medical costs increase with age)

Self-employed individuals looking for tax advantages